Planning for retirement can feel daunting, but securing your future is achievable with the right approach. This ultimate guide to retirement planning provides a comprehensive roadmap to help you navigate the complexities of saving, investing, and managing your finances to achieve your desired retirement lifestyle. Learn strategies to maximize your retirement savings, understand various investment options, and develop a personalized plan tailored to your unique circumstances and financial goals. Discover how to effectively manage your retirement income and ensure a comfortable and secure retirement.

Understanding Retirement Plans

Planning for retirement involves understanding the various types of retirement plans available. These plans differ significantly in how contributions are made, tax implications, and investment options. Choosing the right plan is crucial for securing your financial future.

Defined Benefit Plans (DBPs), also known as pension plans, guarantee a specific monthly payment upon retirement. The employer manages the investments and bears the investment risk. Defined Contribution Plans (DCPs), such as 401(k)s and 403(b)s, require contributions from both the employee and, often, the employer. Investment growth and risk are borne by the employee.

Individual Retirement Accounts (IRAs) offer tax advantages for retirement savings. Traditional IRAs allow pre-tax contributions, while Roth IRAs offer tax-free withdrawals in retirement. Eligibility and contribution limits vary depending on the specific plan.

Understanding the tax implications of each plan is vital. Some plans offer tax deferrals, while others provide tax-free growth or withdrawals. Consider your current tax bracket and anticipated future tax bracket when making your selection. It is highly recommended to consult a financial advisor to determine which plan best suits your individual needs and circumstances.

Importance of Saving Early

The power of compounding is the single most compelling reason to start saving for retirement early. The earlier you begin, the more time your investments have to grow, benefiting from the snowball effect of earning returns on your initial contributions and subsequent earnings. This exponential growth significantly boosts your retirement nest egg.

Starting early also allows you to weather market fluctuations more effectively. Longer time horizons enable you to ride out market downturns, as there’s more opportunity for recovery before retirement. Conversely, those who start later are more vulnerable to market volatility, leaving less time to recover from losses.

Saving early provides greater financial flexibility. Smaller, consistent contributions over a longer period are generally easier to manage than trying to catch up later with larger, more substantial payments. This allows for a more relaxed approach to retirement planning and potentially reduces stress associated with late-stage saving.

Finally, early saving allows for greater control over your retirement lifestyle. The larger your retirement fund, the more options you have regarding your retirement plans—whether it’s early retirement, a comfortable lifestyle, or pursuing passions you may not have had time for during your working years. Essentially, starting early equates to greater financial freedom in retirement.

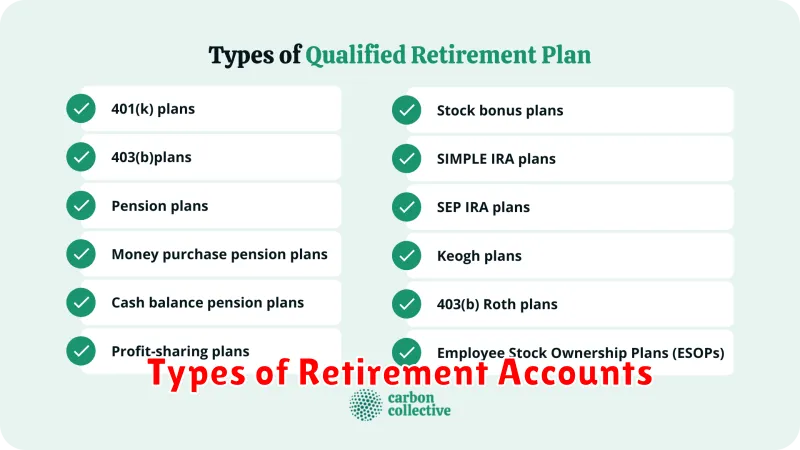

Types of Retirement Accounts

Choosing the right retirement account is crucial for securing your financial future. Several options exist, each with its own advantages and disadvantages. Understanding these differences is key to making informed decisions.

401(k) plans are employer-sponsored retirement savings plans. Contributions are often tax-deferred, meaning you don’t pay taxes on the money until retirement. Many employers offer matching contributions, essentially free money towards your retirement.

Traditional IRAs (Individual Retirement Accounts) allow individuals to contribute a specified amount each year, with contributions often tax-deductible. Taxes are deferred until retirement, similar to a 401(k).

Roth IRAs are also individual retirement accounts, but contributions are made after tax. However, withdrawals in retirement are tax-free, offering a significant advantage.

SEP IRAs (Simplified Employee Pension plans) are designed for self-employed individuals and small business owners. Contributions are tax-deductible, offering a simple way to save for retirement.

Solo 401(k) plans are also for self-employed individuals and small business owners. They offer higher contribution limits than SEP IRAs and allow for both traditional and Roth contributions.

The best retirement account for you will depend on your individual circumstances, income level, and retirement goals. Consulting with a financial advisor can help you determine the most appropriate options.

Tax Implications in Retirement

Retirement planning must consider the significant tax implications impacting your income and assets. Understanding these implications is crucial for maximizing your retirement savings and minimizing your tax burden.

Social Security benefits are subject to taxation depending on your combined income from other sources. Only a portion of your benefits may be taxable, and the amount varies based on individual circumstances.

Retirement account withdrawals, such as from 401(k)s and IRAs, are generally taxed as ordinary income. However, there are strategies to minimize this tax burden, such as Roth IRA conversions or utilizing tax-advantaged withdrawals.

Pension income is usually taxed as ordinary income. Consult a financial advisor to understand how your specific pension plan affects your overall tax liability.

Capital gains taxes can apply to the sale of assets held in taxable accounts. Proper tax planning can help minimize these taxes. Understanding the difference between short-term and long-term capital gains is vital.

Estate taxes may apply to the transfer of assets after death. Estate planning strategies, such as trusts, can help mitigate these taxes.

Tax brackets change over time, and your tax liability in retirement may differ from your current situation. Regularly review your tax situation and consider seeking professional tax advice to optimize your financial strategy and ensure you are adequately prepared.

Investment Strategies for Retirement

Planning for retirement requires a well-defined investment strategy. Your approach should align with your risk tolerance, time horizon, and retirement goals. Consider diversifying your portfolio across various asset classes to mitigate risk.

Stocks offer the potential for higher returns but come with greater volatility. Bonds provide more stability but generally lower returns. A balanced approach, often determined by your age and risk profile, is typically recommended. Younger investors with longer time horizons might allocate more to stocks, while those nearing retirement may shift towards a more conservative bond-heavy portfolio.

Real estate can be a valuable addition, offering potential for both income and appreciation. However, it’s important to understand the inherent illiquidity and management responsibilities involved. Mutual funds and exchange-traded funds (ETFs) offer diversification and professional management, providing convenient access to a wide range of asset classes.

Regularly rebalancing your portfolio is crucial to maintain your desired asset allocation. As market conditions change, some investments may outperform others, causing your portfolio to drift from its target. Rebalancing involves selling some of the better-performing assets and buying more of the underperforming ones to restore the original allocation.

Finally, seeking advice from a qualified financial advisor can be invaluable. They can help you create a personalized strategy tailored to your specific circumstances and assist in navigating the complexities of retirement planning.

Planning for Healthcare in Retirement

Healthcare costs are a significant consideration in retirement planning. Medical expenses can rise dramatically with age, impacting your overall financial security. Careful planning is crucial to mitigate these risks.

Medicare, the federal health insurance program for those 65 and older, is a vital component. However, it doesn’t cover everything. Understanding Medicare’s coverage gaps and supplemental options like Medigap or Medicare Advantage is essential.

Long-term care is another critical aspect. The costs associated with nursing homes or in-home care can be substantial. Consider exploring options like long-term care insurance or setting aside dedicated savings to cover these potential expenses.

Retirement savings should account for projected healthcare costs. Consult with a financial advisor to create a comprehensive plan that incorporates these expenses. Regularly review and adjust your plan as your health needs and financial situation evolve.

Proactive healthcare planning, including preventative care and healthy lifestyle choices, can contribute to lower healthcare costs in the long run. Regular check-ups and maintaining a healthy weight can help prevent costly illnesses down the line.

Creating a Retirement Timeline

Creating a retirement timeline is crucial for effective retirement planning. It provides a visual roadmap, outlining key milestones and deadlines to help you stay on track toward your financial goals.

Begin by determining your desired retirement age. This will be a cornerstone for all subsequent calculations. Consider factors such as health, desired lifestyle, and work preferences.

Next, estimate your retirement expenses. Account for housing, healthcare, travel, and other lifestyle costs. Factor in potential inflation to ensure accuracy.

Calculate the amount of savings needed to support your desired lifestyle in retirement. Utilize online retirement calculators or consult a financial advisor for assistance.

Develop a savings strategy. This involves establishing a realistic savings plan and consistently contributing to retirement accounts like 401(k)s or IRAs. Adjust your contributions as needed based on your progress.

Regularly review and adjust your timeline. Life circumstances change, so periodically reassess your retirement goals, expenses, and savings progress. Make necessary adjustments to your plan as needed.

Consider consulting a financial advisor for personalized guidance and support in creating and maintaining your retirement timeline. They can provide valuable insights and help you navigate the complexities of retirement planning.

{kind=link}