Understanding your creditworthiness goes far beyond simply knowing your credit score. This article delves into the intricacies of credit reports, credit utilization, and the various factors influencing your overall financial health. We’ll explore how to improve your credit history, interpret your credit rating effectively, and ultimately, make informed decisions to achieve your financial goals. Learn how to navigate the complexities of credit management and build a strong foundation for a secure financial future.

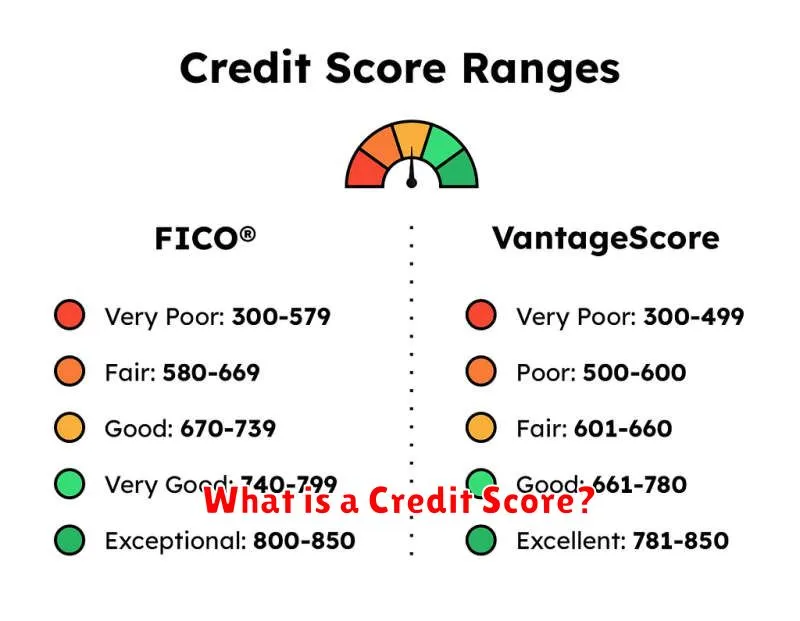

What is a Credit Score?

A credit score is a three-digit number that represents your creditworthiness. It’s a summary of your credit history, reflecting how likely you are to repay borrowed money.

Lenders use credit scores to assess the risk involved in lending you money. A higher score generally indicates lower risk and therefore better loan terms (lower interest rates, higher credit limits).

Several credit bureaus, such as Equifax, Experian, and TransUnion, calculate credit scores using different models, but they all consider similar factors. These factors include your payment history (the most important factor), amounts owed, length of credit history, new credit, and your credit mix (types of credit used).

Your credit score is a crucial element in obtaining loans, mortgages, credit cards, and even renting an apartment. Understanding your score is the first step towards improving your financial health.

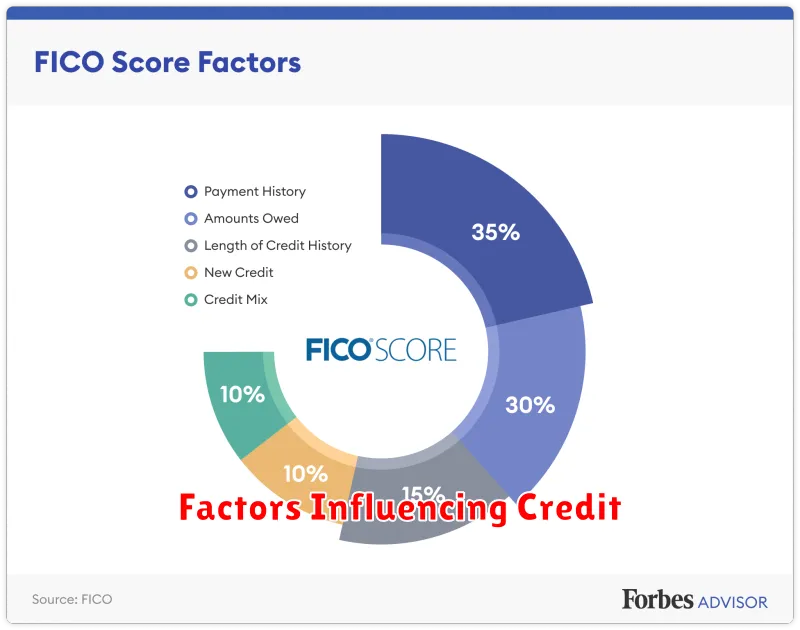

Factors Influencing Credit

Your credit score is a crucial factor in obtaining loans and credit cards, but it’s not the only thing lenders consider. Several other factors significantly influence their lending decisions.

Payment history is paramount. Consistent on-time payments demonstrate financial responsibility. Conversely, late or missed payments negatively impact your creditworthiness.

Amounts owed, or your credit utilization ratio, is another key factor. High balances relative to your available credit limit suggest higher risk to lenders. Maintaining low credit utilization is beneficial.

Length of credit history matters. A longer history of responsible credit management signals stability and reliability. Newer credit profiles might present higher risk.

The types of credit you utilize also play a role. A diverse credit portfolio (e.g., credit cards, installment loans, mortgages) can positively influence your credit assessment.

Finally, new credit applications can temporarily lower your credit score. Multiple applications in a short period indicate a higher risk of potential debt overload for the lender.

Improving Your Credit

Improving your credit score requires consistent effort and responsible financial behavior. Focus on paying all your bills on time; this is the single most important factor impacting your score.

Keep your credit utilization ratio low. This refers to the amount of credit you’re using compared to your total available credit. Aim to keep it below 30%, ideally much lower.

Maintain a diverse mix of credit accounts, demonstrating responsible management of different credit types (credit cards, installment loans). However, avoid opening too many new accounts in a short period.

Check your credit report regularly for errors. Dispute any inaccuracies you find with the respective credit bureaus.

Consider strategies like paying down high-interest debt first, as high balances can negatively affect your score. Be patient and persistent; improving your credit takes time.

If you’re struggling, consider seeking guidance from a non-profit credit counseling agency to help you create a plan.

Credit Utilization Explained

Credit utilization is the ratio of your outstanding credit card debt to your total available credit. It’s expressed as a percentage.

For example, if you have a $10,000 credit limit and owe $2,000, your credit utilization is 20% ( $2,000 / $10,000 x 100%).

Keeping your credit utilization low (ideally below 30%, and preferably below 10%) is crucial for a good credit score. High credit utilization indicates a greater reliance on credit and suggests a higher risk to lenders.

Factors affecting credit utilization include your spending habits, available credit lines, and repayment frequency. Regularly paying down your balances and managing your credit responsibly can significantly improve your credit utilization ratio.

Monitoring your credit utilization is essential for maintaining a healthy credit profile. Regularly checking your credit reports and paying down balances promptly helps you stay on top of your credit utilization and improve your creditworthiness.

Building a Credit History

Establishing a credit history is crucial for accessing various financial products and services. A strong credit history demonstrates your reliability in managing debt. This history is built over time through responsible credit use.

One of the primary ways to build credit is by obtaining a secured credit card. These cards require a security deposit, reducing the lender’s risk. Consistent, on-time payments on this card will begin to build your credit profile.

Another option is becoming an authorized user on someone else’s credit card account. If the primary account holder has a good payment history, their positive credit activity can positively impact your credit report, provided they allow you to be listed.

Taking out a loan, such as a small personal loan or student loan, can also contribute to building credit. Again, consistent on-time payments are key. Remember to borrow responsibly and only take out loans you can afford to repay.

Finally, ensuring your credit report is accurate is vital. Regularly review your credit report for any errors and dispute any inaccuracies with the relevant credit bureaus. A clean and accurate credit report is foundational to building good credit.

Impact of Credit on Loans

Your credit score significantly impacts your ability to secure loans and the terms you’ll receive. A higher score demonstrates creditworthiness, leading to better loan offers.

Lenders use your credit report to assess risk. A strong credit history, reflected in a high score, indicates a lower risk of default, resulting in lower interest rates and potentially more favorable loan terms, such as longer repayment periods.

Conversely, a low credit score signifies higher risk. This often translates to higher interest rates, smaller loan amounts, and potentially stricter lending criteria. In some cases, a poor credit history can even lead to loan applications being denied.

Therefore, maintaining a healthy credit score is crucial for accessing favorable loan options. Understanding your credit report and actively managing your credit is essential for securing the best possible loan terms.

Monitoring Your Credit

Regularly monitoring your credit reports is crucial for maintaining a healthy credit profile. This involves checking your reports from each of the three major credit bureaus: Equifax, Experian, and TransUnion, at least annually.

Errors can significantly impact your credit score, so reviewing your reports for inaccuracies is vital. These errors could include incorrect account information, late payments that weren’t yours, or accounts that don’t belong to you. Disputing these errors promptly is key to correcting your credit history.

Beyond error detection, monitoring allows you to track your credit utilization ratio – the amount of credit you’re using compared to your total available credit. Keeping this ratio low (ideally below 30%) is essential for a positive credit score.

Furthermore, monitoring provides early warning signs of potential identity theft. Unexpected accounts or inquiries can indicate fraudulent activity, allowing you to take immediate action to protect your financial well-being.

Utilizing free credit monitoring services offered by credit bureaus or financial institutions is a cost-effective way to maintain consistent oversight of your credit reports. This proactive approach safeguards your credit and helps you achieve your financial goals.

Common Credit Myths

Many misconceptions surround credit scores and management. One common myth is that checking your credit score hurts your credit. This is false; checking your own score through authorized channels, like your bank or a credit monitoring service, has no negative impact.

Another prevalent myth is that paying only the minimum payment is sufficient. While it avoids late fees, consistently paying only the minimum keeps you in debt longer and accrues significantly more interest, harming your credit score in the long run. Paying more than the minimum is crucial for healthy credit.

It’s also a misconception that closing old credit cards improves your credit score. While it might seem logical, older accounts, even if unused, contribute to your credit history length, a positive factor in credit scoring. Closing them can negatively impact your credit utilization ratio.

Finally, many believe that only large purchases affect credit. While large purchases do impact your credit utilization, all credit transactions, big or small, are recorded and contribute to your credit profile. Consistent, responsible spending habits are essential for a strong credit score.

{kind=link}