Unlock the secrets to credit card mastery and transform your spending habits into substantial rewards. This comprehensive guide will equip you with the proven strategies to maximize your credit card rewards, from choosing the right card for your spending patterns to strategically utilizing points and miles for unforgettable travel experiences and valuable merchandise. Learn how to avoid credit card debt while simultaneously reaping the benefits of lucrative rewards programs. Discover the power of credit cards when used responsibly and effectively.

Understanding Credit Card Basics

Understanding the fundamentals of credit cards is crucial for maximizing rewards. A credit card allows you to borrow money from a lender (the card issuer) to make purchases, promising to repay the borrowed amount plus interest later.

Credit Limit: This is the maximum amount you’re allowed to borrow. Using more than your credit limit results in penalties.

Interest Rate (APR): This is the annual percentage rate you pay on your outstanding balance if you don’t pay it in full each month. Lower APRs are more favorable.

Minimum Payment: The smallest amount you can pay each month to avoid late fees. Paying only the minimum will result in paying significantly more interest over time.

Grace Period: The time you have to pay your balance in full without incurring interest charges. This typically ranges from 21 to 25 days.

Statement: A monthly summary of your transactions, payments, and outstanding balance. Reviewing your statement regularly is key to managing your spending and avoiding errors.

Credit Score Impact: Responsible credit card use (paying on time, keeping balances low) helps build a strong credit score, impacting your ability to get loans and other financial products at favorable rates.

Rewards Programs: Many credit cards offer rewards, such as cashback, points, or miles, on purchases. Understanding the terms and conditions of these programs is critical for maximizing benefits.

Reward Programs Explained

Credit card reward programs offer various ways to earn rewards for your spending. Points, miles, and cash back are the most common types. Each program has its own rules and earning rates.

Points are typically earned at a fixed rate per dollar spent and can be redeemed for travel, merchandise, or cash back. Miles are specifically designed for travel rewards, often offering redemption for flights and hotel stays. Cash back programs directly reward you with a percentage of your spending, usually credited to your account.

Understanding the terms and conditions of each program is crucial. Pay close attention to the earning rates, redemption options, and any annual fees or expiration dates associated with the rewards.

Some programs offer bonus categories, providing increased earning rates on specific purchases like groceries or gas. Others feature welcome bonuses offering a substantial initial reward upon card activation. Redemption value varies greatly, so compare how many points/miles are needed for a specific reward.

Effectively using reward programs involves strategic spending habits. Focus your spending on categories that maximize your earnings. Choosing the right card for your spending habits is key to maximizing rewards.

Comparing Credit Card Offers

Choosing the right credit card requires careful comparison of various offers. Focus on the annual fee; a high fee may negate rewards unless spending significantly exceeds the fee.

Interest rates (APR) are crucial if you carry a balance. Compare APRs across different cards and ensure you understand the terms. A lower APR is always preferable.

Rewards programs vary significantly. Consider whether you value cash back, points, or miles. Evaluate the earning rate (e.g., 2% cash back) and the redemption value of the rewards.

Examine the bonus offers. Many cards offer substantial sign-up bonuses; however, be mindful of the spending requirements needed to achieve these. Consider the timeframe needed to meet the requirements.

Additional benefits, such as travel insurance, purchase protection, or extended warranties, can add value. Consider which benefits align with your spending habits and lifestyle.

Use online comparison tools to streamline the process. These tools allow you to input your spending habits to identify cards that best suit your needs. Remember to always read the fine print before applying.

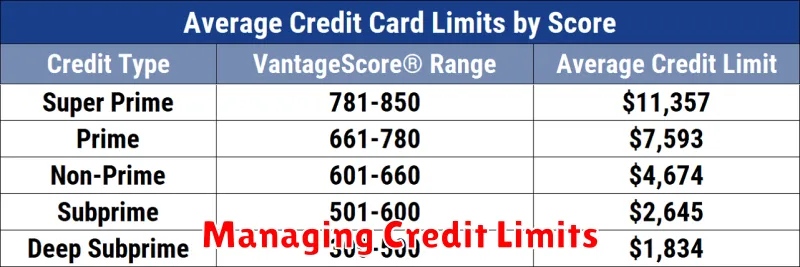

Managing Credit Limits

Credit limit management is crucial for maximizing rewards and maintaining a healthy credit score. Understanding your credit limit – the maximum amount you can borrow – is the first step.

Avoid maxing out your cards. Keeping your credit utilization ratio (the percentage of your available credit you’re using) low (ideally below 30%) is vital for a good credit score. High utilization suggests financial strain and can negatively impact your creditworthiness.

Request credit limit increases strategically. A higher limit can boost your credit utilization ratio, making it easier to stay below the 30% threshold. However, only request an increase if you can confidently manage the additional credit responsibly.

Monitor your credit report regularly. Check for any errors and ensure your credit limit information is accurate. Regular monitoring helps you stay informed about your credit health.

Consider a balance transfer if you have high-interest debt on other cards. This can help you manage your debt more effectively and potentially lower your interest payments, freeing up more money for rewards-earning purchases.

Responsible credit limit management is key to maximizing rewards and building a strong financial foundation. By carefully monitoring your spending and credit utilization, you can optimize your credit card usage for greater benefits.

Building Credit History

Building a strong credit history is crucial for maximizing rewards with credit cards. Lenders assess your creditworthiness based on your history, influencing interest rates and credit limits offered.

Start by obtaining a secured credit card. These cards require a security deposit that acts as your credit limit, minimizing lender risk. Responsible use, such as paying your balance in full and on time, will demonstrate creditworthiness.

Consider becoming an authorized user on a family member or friend’s credit card with a good history. Their positive payment history can positively impact your credit score, provided they maintain excellent credit habits. However, be sure to carefully review the agreement.

Another strategy is to apply for a credit-builder loan. These loans are specifically designed to help you establish credit. Consistent on-time payments build your credit history, while regular reporting to credit bureaus ensures your progress is reflected accurately.

Monitoring your credit report regularly is vital. Review your report for accuracy and identify any potential issues promptly. Regular monitoring allows for proactive identification of any errors or fraudulent activity.

Finally, maintain a low credit utilization ratio. This represents the percentage of available credit you use. Keeping it below 30% demonstrates responsible credit management and enhances your credit score.

Avoiding Common Pitfalls

One major pitfall is carrying a balance. High interest rates negate any rewards earned. Always pay your balance in full and on time to avoid accumulating debt.

Another common mistake is applying for too many cards too quickly. This can negatively impact your credit score, hindering your ability to secure favorable credit terms in the future. Focus on a few strategically chosen cards instead.

Ignoring the terms and conditions is a critical error. Carefully review the fee structure, interest rates, and reward programs of each card to ensure they align with your spending habits and financial goals. Understand the nuances of reward redemption processes to maximize your benefits.

Finally, forgetting to track your spending and rewards can lead to missed opportunities. Regularly monitor your account activity to ensure you’re maximizing rewards and identify potential areas for improvement in your spending habits.

Strategies for Maximizing Rewards

Understanding your card’s rewards program is crucial. Carefully review the terms and conditions to understand earning rates, bonus categories, and redemption options. Many cards offer bonus rewards for spending in specific categories, such as groceries or travel. Maximize these by concentrating your spending in those categories.

Strategic spending is key. Plan your purchases to align with your card’s rewards structure. If your card offers increased rewards on dining, prioritize dining expenses on that card. Consider using a different card for other purchases that offer better returns.

Meeting spending minimums for welcome bonuses can significantly boost your rewards. While it’s important to avoid unnecessary spending, if you can reasonably reach the minimum spending requirement within the promotional period, the bonus points or cash back can be substantial.

Redeeming rewards wisely is essential. Compare the value of different redemption options. Sometimes, redeeming for travel or merchandise can yield higher value than a simple cash-back payout. Consider the value of your points or miles when making redemption decisions.

Tracking your spending and rewards is vital for staying organized and maximizing your earnings. Utilize the card’s online portal or a budgeting app to monitor your progress and ensure you’re making the most of your rewards program.

{kind=link}