Understanding the intricacies of loans can feel daunting, but it’s a crucial step before taking on any debt. This article will equip you with the essential knowledge to navigate the world of personal loans, business loans, and other types of financing. We’ll explore key concepts such as interest rates, loan terms, credit scores, and repayment strategies, empowering you to make informed decisions and secure the best possible loan for your specific needs. Learn how to compare loan offers, avoid hidden fees, and protect your financial future before you borrow.

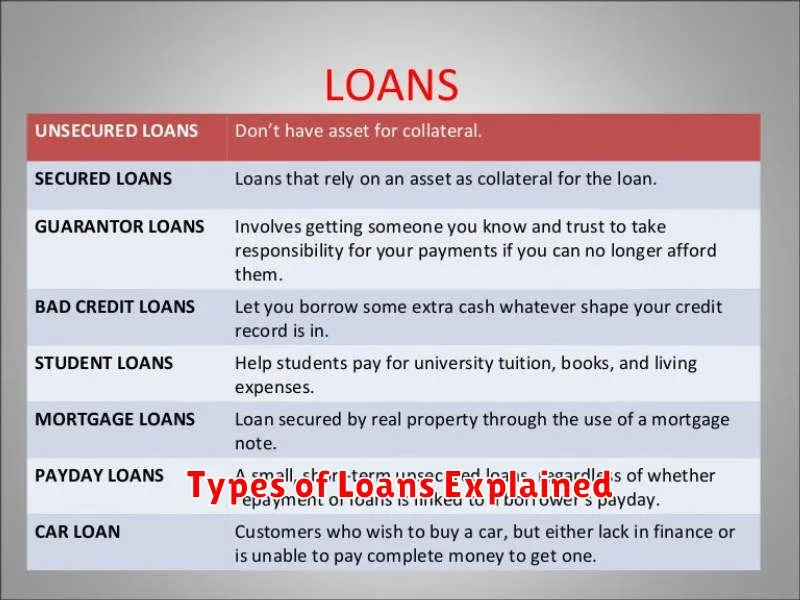

Types of Loans Explained

Understanding the various types of loans available is crucial before borrowing. Different loans cater to different needs and come with varying terms and conditions. Choosing the right loan depends heavily on your specific financial situation and purpose.

Secured loans require collateral, an asset like a house or car, to secure the loan. If you default, the lender can seize the collateral. Examples include mortgages (for real estate) and auto loans. Secured loans typically offer lower interest rates due to the reduced risk for the lender.

Unsecured loans, conversely, don’t require collateral. They rely on your creditworthiness. Examples include personal loans and credit cards. Unsecured loans usually have higher interest rates because of the increased risk for the lender.

Payday loans are short-term, high-interest loans designed to be repaid on your next payday. These loans should be approached with extreme caution due to their extremely high interest rates and potential for a debt cycle.

Student loans are specifically designed to finance education. They typically have lower interest rates than other unsecured loans and offer repayment plans tailored to graduates’ income.

Business loans are used to fund business operations, expansions, or equipment purchases. These can be secured or unsecured and are often based on the business’s financial health and credit history.

Each loan type has its own pros and cons. Carefully consider your financial needs, repayment capacity, and the terms offered before committing to any loan.

How to Choose the Right Loan

Choosing the right loan depends heavily on your specific needs and financial situation. Consider the purpose of the loan – is it for a home, a car, or debt consolidation? This will influence the type of loan you should seek.

Carefully compare interest rates from different lenders. A lower interest rate will save you money over the life of the loan. Also, examine the loan term; a shorter term means higher monthly payments but less interest paid overall, while a longer term offers lower monthly payments but higher total interest.

Understand all fees associated with the loan, including origination fees, prepayment penalties, and late payment fees. These can significantly impact the overall cost. Review the loan’s terms and conditions thoroughly before signing any agreement. Consider seeking professional financial advice if you need assistance in understanding the complexities of different loan options.

Finally, ensure you can comfortably afford the monthly payments. Calculate your debt-to-income ratio (DTI) to determine your borrowing capacity. Don’t borrow more than you can realistically repay, as this can lead to financial hardship.

Interest Rates and Loan Terms

Interest rates are a crucial aspect of any loan. They represent the cost of borrowing money, expressed as a percentage of the principal loan amount. A higher interest rate means you’ll pay more in interest over the life of the loan. Lower interest rates result in lower overall costs.

Loan terms define the repayment schedule, specifying the loan duration (e.g., 12 months, 36 months, or longer) and the frequency of payments (e.g., monthly, quarterly). A shorter loan term typically means higher monthly payments but less interest paid overall. Conversely, a longer loan term results in lower monthly payments but higher total interest paid.

Understanding the interplay between interest rates and loan terms is vital. A lower interest rate can offset the impact of a longer loan term, and vice-versa. Borrowers should carefully compare offers with different interest rates and loan terms to find the most financially suitable option. Factors influencing interest rates include credit score, loan amount, and the type of loan.

Application Process Demystified

The loan application process can seem daunting, but understanding the steps involved simplifies it significantly. It generally begins with pre-qualification, where you provide basic financial information to get an estimate of how much you might borrow and at what interest rate. This doesn’t impact your credit score.

Next comes the formal application. This requires more detailed information, including your income, employment history, debts, and credit score. Lenders will pull your credit report, so ensuring your credit is in good standing is crucial. Be prepared to provide supporting documentation such as pay stubs, tax returns, and bank statements.

Following the application, the lender will review your information and assess your creditworthiness. This may involve further questions or requests for additional documentation. If approved, you’ll receive a loan offer detailing the terms, including interest rates, fees, and repayment schedule. Carefully review this before accepting.

Finally, closing the loan involves signing the loan agreement and receiving the funds. Understanding the terms and conditions of your loan is vital before finalizing the agreement. Remember to ask questions if anything is unclear.

Credit Score and Loan Approval

Your credit score is a crucial factor in loan approval. Lenders use it to assess your creditworthiness – your ability to repay borrowed funds. A higher credit score generally indicates a lower risk to the lender, increasing your chances of approval and potentially securing you a better interest rate.

A good credit score typically translates to easier loan approval, more favorable terms, and lower interest rates. Conversely, a poor credit score can make it difficult to get approved for a loan, or it may result in higher interest rates and less favorable terms if you are approved.

Factors affecting your credit score include payment history, amounts owed, length of credit history, new credit, and credit mix. Improving your credit score before applying for a loan can significantly improve your chances of approval.

It’s important to check your credit report for any inaccuracies before applying for a loan. Dispute any errors you find to ensure an accurate reflection of your credit history. Remember that lenders may also consider other factors beyond your credit score when making a loan decision, including your income and debt-to-income ratio.

Managing Loan Repayments

Effective loan repayment hinges on careful planning and proactive management. Begin by understanding your loan agreement, paying close attention to the repayment schedule, interest rate, and any fees. Create a budget that allocates sufficient funds for your monthly payments, ensuring it’s a priority alongside other essential expenses.

Consider setting up automatic payments to avoid late fees and maintain a positive payment history. This simplifies the process and reduces the risk of missed payments. Regularly review your loan statement to track your progress and identify any discrepancies. If you anticipate difficulty meeting a payment, contact your lender immediately to explore options like forbearance or refinancing.

Maintaining open communication with your lender is crucial. They can offer guidance and potentially work with you to avoid default. Prioritizing timely repayments is essential to building a strong credit history, which impacts future borrowing opportunities. Remember that responsible loan management reduces financial stress and improves your overall financial well-being.

Tips for Borrowers

Before taking out a loan, carefully compare interest rates from multiple lenders. A seemingly small difference in interest can significantly impact your total repayment cost.

Understand the loan terms thoroughly. Read the fine print and clarify any uncertainties with the lender before signing the agreement. Pay close attention to repayment schedules, fees, and penalties for late payments.

Assess your ability to repay the loan. Create a realistic budget that accounts for the monthly loan payment, alongside your other financial obligations. Avoid borrowing more than you can comfortably afford.

Consider the type of loan that best suits your needs. Different loan types (e.g., personal loans, auto loans, mortgages) have varying interest rates, terms, and eligibility requirements. Choose wisely based on your financial situation and purpose of borrowing.

Shop around for the best deal. Don’t settle for the first offer you receive. Compare offers from various lenders to find the most favorable terms and conditions. This can save you considerable money in the long run.

Maintain good credit. A strong credit score can significantly improve your chances of loan approval and securing a lower interest rate. Consistent on-time payments contribute to a better credit history.

{kind=link}