Planning for a secure retirement is crucial, and understanding effective retirement savings strategies is paramount. This article delves into actionable steps to help you build a robust retirement plan, covering topics such as retirement accounts (like 401(k)s and IRAs), investment strategies for growth and preservation, and navigating retirement planning challenges. Learn how to maximize your retirement savings and achieve financial security in your golden years.

Planning Your Retirement

Planning for retirement requires a proactive approach and careful consideration of several key factors. Begin by estimating your retirement expenses, considering factors like housing, healthcare, and leisure activities. This will help determine your necessary savings goal.

Determine your retirement timeline. Knowing when you plan to retire will influence your savings strategy and allow for adjustments based on your age and time horizon. A longer timeline allows for more aggressive investment strategies while shorter timelines may require more conservative approaches.

Develop a comprehensive savings plan encompassing various retirement vehicles. Consider utilizing employer-sponsored retirement plans like 401(k)s or 403(b)s, maximizing employer matching contributions. Supplement these with individual retirement accounts (IRAs), such as traditional or Roth IRAs, depending on your tax bracket and long-term financial goals.

Regularly review and adjust your plan. Life circumstances change, so it’s crucial to periodically assess your progress, make necessary adjustments, and ensure your plan aligns with your evolving needs and goals. Consider consulting with a financial advisor for personalized guidance.

Diversify your investments to mitigate risk. Don’t put all your eggs in one basket. Spread your investments across different asset classes to balance potential returns with risk tolerance.

Understanding Retirement Accounts

Retirement accounts are specifically designed to help individuals save for their retirement years. They offer significant tax advantages, encouraging long-term savings and growth. Understanding the different types is crucial for effective retirement planning.

401(k) plans are employer-sponsored retirement savings plans. Employees contribute a portion of their pre-tax salary, often with employer matching contributions. These contributions grow tax-deferred, meaning taxes are paid only upon withdrawal in retirement.

Traditional IRAs (Individual Retirement Accounts) allow individuals to contribute pre-tax dollars annually, up to a certain limit. Earnings grow tax-deferred, and withdrawals in retirement are taxed as income. Roth IRAs differ; contributions are made after tax, but qualified withdrawals in retirement are tax-free.

SEP IRAs (Simplified Employee Pension plans) are retirement plans for self-employed individuals and small business owners. Contributions are made pre-tax, and withdrawals are taxed in retirement.

Choosing the right retirement account depends on individual circumstances, including income level, employer benefits, and risk tolerance. Careful consideration of contribution limits, tax implications, and investment strategies is essential for maximizing retirement savings.

Saving Early for Retirement

Starting your retirement savings early offers a significant advantage due to the power of compound interest. Even small, regular contributions made early in your career can accumulate substantially over time, significantly reducing the burden of saving later in life.

The earlier you begin, the more time your money has to grow exponentially. This allows you to invest more aggressively, potentially taking on higher risks with higher potential returns, while still having sufficient time to recover from any market downturns.

Early saving also provides greater flexibility. You can adjust your savings strategy as needed, based on life changes, without needing to drastically increase contributions later to achieve your goals. It allows for a more relaxed approach to retirement planning.

Consider utilizing tax-advantaged accounts like 401(k)s and IRAs to maximize your savings potential and minimize your tax burden. Automatic contributions can simplify the process and ensure consistent saving.

In short, initiating retirement savings early is a crucial step toward securing a comfortable and financially independent retirement. The benefits of compounding interest, flexibility, and reduced future burden are substantial and well worth the effort.

Investment Options for Retirement

Choosing the right investment options for retirement is crucial for securing your financial future. Several options cater to different risk tolerances and financial goals.

Stocks offer the potential for high returns but carry higher risk. Bonds generally provide lower returns but are less volatile. A diversified portfolio, combining both, can help balance risk and reward.

Mutual funds and exchange-traded funds (ETFs) offer diversification by pooling investments in various assets. Real estate can be a valuable long-term investment, although it requires more management.

Annuities provide a guaranteed income stream in retirement, but often come with fees and limitations on access to funds. Retirement accounts such as 401(k)s and IRAs offer tax advantages, making them attractive options for retirement savings.

It’s essential to consult with a financial advisor to determine the best investment strategy based on your individual circumstances, risk tolerance, and retirement goals. Consider your time horizon; longer time horizons allow for greater risk-taking.

Tax Benefits and Retirement

Planning for retirement involves strategic saving and leveraging available tax advantages. These benefits can significantly boost your retirement nest egg.

Many retirement accounts, such as 401(k)s and Traditional IRAs, offer tax-deferred growth. This means you don’t pay taxes on your investment earnings until retirement, allowing your savings to compound faster.

Roth IRAs, conversely, offer tax-free withdrawals in retirement after a specific period. Contributions are made after tax, but qualified withdrawals are tax-free, providing a significant advantage in retirement.

Tax credits and deductions can also reduce your current tax liability, freeing up more money for retirement savings. Eligibility varies based on income and other factors, so it’s important to research the specific options available to you.

Understanding and utilizing these tax benefits is crucial for maximizing your retirement savings and ensuring a more secure financial future.

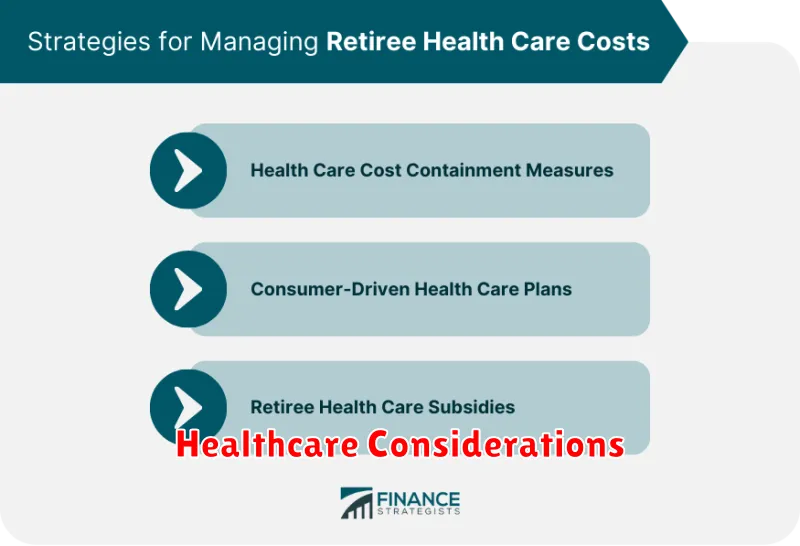

Healthcare Considerations

Healthcare costs are a significant and often underestimated expense in retirement. Planning for these costs is crucial to ensuring a secure financial future.

Medicare, while helpful, doesn’t cover all medical expenses. Supplementary insurance like Medicare Advantage or Medigap can help bridge the gap, but these also carry costs.

Long-term care, including nursing homes or assisted living, is exceptionally expensive. Consider the potential need for this and explore options like long-term care insurance or setting aside a dedicated savings fund.

Prescription drug costs can also be substantial. Review your current medications and research potential savings through prescription drug discount cards or negotiating lower prices.

Regular health checkups and preventative care can help reduce healthcare costs in the long run. These measures often prevent more serious and expensive medical issues down the line. Building healthy habits earlier in life pays off significantly.

Consider consulting with a financial advisor specializing in retirement planning to create a personalized strategy that incorporates your individual healthcare needs and risk tolerance. This professional guidance can be invaluable in navigating the complexities of healthcare costs during retirement.

Retirement Lifestyle Planning

Retirement lifestyle planning is crucial for ensuring a comfortable and fulfilling retirement. It involves carefully considering your desired lifestyle and aligning it with your financial resources. This includes assessing your housing needs, healthcare expenses, travel aspirations, and hobbies.

Budgeting is a key component. You need to project your monthly expenses in retirement, factoring in inflation and potential unexpected costs. This will help you determine the required retirement savings and potentially identify areas where adjustments can be made to your lifestyle preferences.

Healthcare costs often represent a significant portion of retirement expenses. It’s essential to understand your health insurance options and plan for potential long-term care needs. Estate planning should also be considered, encompassing wills, trusts, and power of attorney to ensure your assets are distributed according to your wishes.

Regularly reviewing and adjusting your retirement plan is vital, as circumstances and priorities may change over time. Consider seeking professional advice from a financial advisor to personalize your strategy and ensure you’re on track to achieve your desired retirement lifestyle.

Adjusting Your Savings Strategy

Life changes necessitate adjustments to your retirement savings strategy. Unexpected events, such as job loss or medical emergencies, can significantly impact your savings plan. Regularly reviewing and adapting your strategy is crucial.

Re-evaluating your goals is a key aspect of adjustment. Changes in lifestyle expectations, health considerations, or family circumstances may require you to reassess your target retirement income and adjust your savings accordingly. Consider using online retirement calculators to project your needs based on your updated circumstances.

Investment adjustments are also important. Market fluctuations and your risk tolerance shift over time. Periodically review your investment portfolio to ensure it aligns with your revised timeline and risk appetite. Consider consulting a financial advisor for personalized guidance on asset allocation.

Monitoring your progress is essential for maintaining a successful strategy. Regularly track your savings, assess your progress against your goals, and make adjustments as needed. This proactive approach ensures you stay on track to achieve a secure retirement.

Finally, remember that flexibility is paramount. Your retirement savings strategy shouldn’t be static. Be prepared to adapt your plan as life throws curveballs, ensuring you are always working towards a comfortable and secure future.

Long-term Financial Security

Achieving long-term financial security in retirement requires a proactive and well-structured savings plan. This involves more than simply saving; it necessitates a comprehensive strategy encompassing various elements.

Diversification is crucial. Spreading investments across different asset classes (stocks, bonds, real estate, etc.) helps mitigate risk and maximize potential returns over the long term. Regular contributions, even small ones, compound significantly over time due to the power of compound interest.

Careful budgeting and disciplined saving are essential foundations. Regularly reviewing and adjusting your budget ensures you’re allocating sufficient funds towards retirement savings while managing current expenses. Understanding your risk tolerance and aligning your investment strategy accordingly is vital for long-term success.

Finally, seeking professional financial advice can prove invaluable. A financial advisor can help you create a personalized plan tailored to your specific circumstances, goals, and risk profile, enhancing your prospects for long-term financial security and a comfortable retirement.

{kind=link}