This comprehensive guide to personal loans will equip you with the knowledge to make informed decisions about securing financing for your needs. We’ll explore various loan types, interest rates, repayment options, and crucial factors to consider before applying for a personal loan. Learn how to compare offers, improve your chances of approval, and understand the responsibilities involved in managing your debt effectively. Whether you’re considering a personal loan for debt consolidation, home improvements, or other significant expenses, this guide provides essential insights into the entire loan process.

Introduction to Personal Loans

A personal loan is an unsecured or secured loan from a financial institution, such as a bank or credit union, that provides a borrower with a lump sum of money. This money can be used for various purposes, unlike loans with a specific designation, such as a mortgage or auto loan.

Key features of personal loans often include a fixed repayment schedule (typically monthly installments), a fixed interest rate (though some may offer variable rates), and a predetermined loan term (the length of time to repay the loan). The interest rate offered will vary based on the borrower’s creditworthiness, the loan amount, and the repayment term.

Personal loans can be used for a wide variety of needs, including debt consolidation, home improvements, medical expenses, or unexpected emergencies. The application process generally involves submitting an application, providing financial information, and undergoing a credit check. Approval depends on several factors, primarily your credit score and debt-to-income ratio.

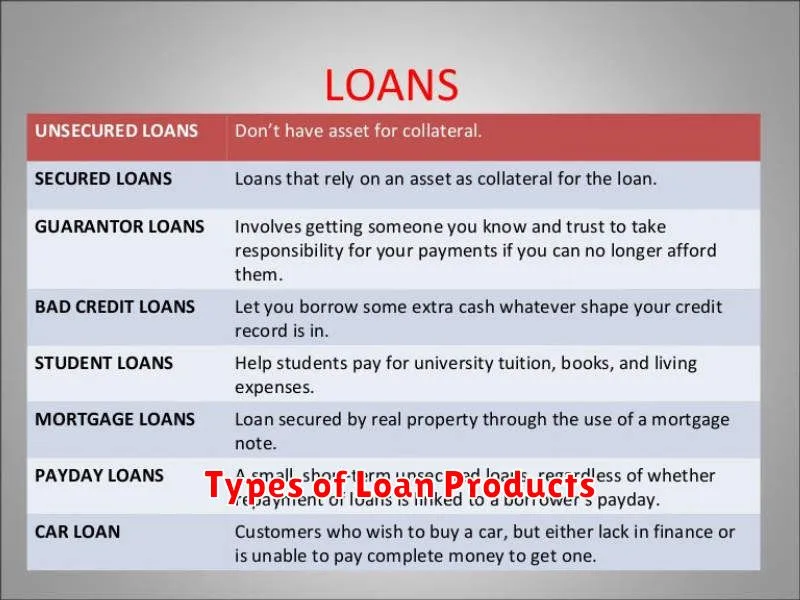

Types of Loan Products

Personal loans come in various forms, each designed to cater to different needs and financial situations. Unsecured personal loans, the most common type, don’t require collateral. Your creditworthiness is the primary factor determining approval and interest rates. Secured personal loans, conversely, require collateral, such as a car or savings account, to back the loan. This typically results in lower interest rates but carries the risk of losing the collateral if the loan isn’t repaid.

Debt consolidation loans are specifically designed to consolidate multiple debts into a single, manageable monthly payment. This can simplify repayment and potentially lower interest rates, but it’s crucial to evaluate the terms carefully. Peer-to-peer (P2P) loans connect borrowers directly with lenders, often offering competitive interest rates but requiring a strong credit history for approval. Finally, Payday loans are short-term, high-interest loans intended to bridge the gap until your next paycheck. They should be used cautiously due to their high cost.

The type of personal loan best suited to you will depend on your credit score, financial situation, and the purpose of the loan. Carefully compare interest rates, fees, and repayment terms before making a decision. Understanding the differences between these loan products is crucial for choosing the option that best aligns with your individual circumstances and financial goals.

Interest Rates and Fees

Interest rates are a crucial aspect of personal loans. They represent the cost of borrowing money, expressed as a percentage of the principal loan amount. Lower rates result in lower overall costs. The rate offered depends on several factors including your credit score, loan amount, and the lender’s current market conditions.

Beyond interest, fees can significantly impact the total cost. Common fees include origination fees (charged upfront for processing the loan), prepayment penalties (for paying off the loan early), and late payment fees (for missed payments). Carefully review all fees before accepting a loan to understand the full financial commitment.

Annual Percentage Rate (APR) is a key figure that combines the interest rate and most fees to provide a complete picture of the loan’s true cost. Comparing APRs from multiple lenders is essential to find the most affordable option. Always prioritize transparency regarding fees and interest rates to avoid unexpected costs.

Loan Application Process

The personal loan application process typically begins with pre-qualification. This involves providing basic information to receive an estimated loan amount and interest rate without impacting your credit score. This helps you determine your eligibility and desired loan terms.

Next is the formal application. You’ll need to complete a detailed application form, providing personal details, employment history, income, and expenses. Be prepared to provide supporting documentation such as pay stubs, tax returns, and bank statements to verify your financial information.

The lender then conducts a credit check to assess your creditworthiness. A strong credit history increases your chances of approval and may lead to more favorable interest rates. This process may take a few business days.

Following the credit check, the lender will review your application and supporting documents. If approved, you’ll receive a loan offer outlining the terms, including the interest rate, loan amount, repayment schedule, and any associated fees.

Finally, upon acceptance of the loan offer, you’ll sign the loan agreement and receive the loan funds, typically deposited directly into your bank account. It is crucial to carefully review all loan terms and conditions before signing the agreement.

Credit Score Impact

Applying for a personal loan can impact your credit score, both positively and negatively. A hard inquiry, made when you apply, can slightly lower your score temporarily. However, responsible repayment of the loan can significantly improve your credit score over time by demonstrating your creditworthiness. Factors influencing the impact include your existing credit history, credit utilization, and the loan’s terms.

Regular on-time payments are crucial. Missed or late payments can severely damage your credit score and negatively affect your ability to secure future loans or credit. Conversely, consistently making timely payments will build a positive credit history, leading to a higher credit score and potentially better loan terms in the future.

The type of loan also matters. Secured loans (backed by collateral) might have less of an impact than unsecured loans, depending on your credit profile. Before applying, consider your current credit score and how a personal loan might influence it. Shop around and compare offers to find the best loan terms for your financial situation.

Managing Loan Repayment

Effective loan repayment requires careful planning and discipline. Begin by understanding your loan agreement, noting the repayment schedule, including the monthly payment amount, due date, and total interest. This information is crucial for budgeting and avoiding late payments.

Budgeting is paramount. Allocate a specific amount from your monthly income towards your loan repayment. Consider using automated payments to ensure timely and consistent contributions. This automated system helps avoid missed payments and associated penalties.

Explore options for reducing your loan term. While this may increase your monthly payments, it significantly lowers the total interest paid over the loan’s lifespan, saving you money in the long run. Consider making extra payments whenever possible to accelerate repayment.

Maintain open communication with your lender. Contact them immediately if you anticipate difficulties meeting your repayment obligations. They may offer options such as deferment or repayment plans to help you manage your debt effectively.

Finally, tracking your progress is essential. Regularly monitor your loan balance and ensure your payments are accurately reflected. This proactive approach empowers you to stay on track and achieve timely loan repayment.

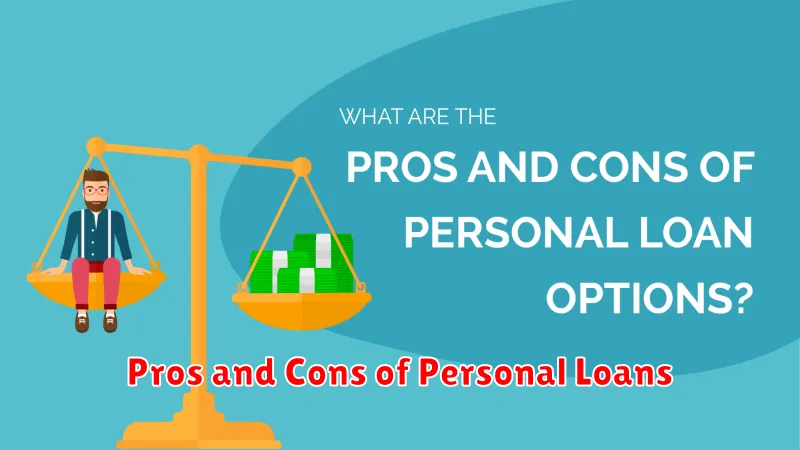

Pros and Cons of Personal Loans

Personal loans offer several advantages. They provide a lump sum of money that can be used for various purposes, such as debt consolidation, home improvements, or medical expenses. The repayment terms are typically fixed and predictable, making budgeting easier. Furthermore, interest rates can be lower than those on credit cards, leading to potential cost savings. Secured personal loans often come with lower interest rates than unsecured loans.

However, personal loans also have disadvantages. Borrowers need to meet specific credit score requirements, and those with poor credit may face higher interest rates or loan denial. Missing payments can severely damage credit scores and lead to additional fees. The fixed repayment schedule can be challenging for individuals with fluctuating incomes. Finally, interest charges can accumulate significantly over the loan term, increasing the overall cost.

Tips for Loan Approval

Securing a personal loan hinges on presenting yourself as a low-risk borrower to the lender. This involves demonstrating a strong financial profile.

Maintain a high credit score. A good credit history significantly improves your chances of approval and can even secure you a better interest rate. Check your credit report regularly and address any inaccuracies.

Keep your debt-to-income ratio (DTI) low. Lenders assess your ability to repay by comparing your debts to your income. A lower DTI indicates a greater capacity to manage loan repayments.

Provide accurate and complete information on your loan application. Inaccuracies or omissions can lead to rejection. Be prepared to support your application with necessary documentation.

Shop around for the best loan terms. Different lenders offer varying interest rates and fees. Comparing offers enables you to secure the most favorable loan.

Consider a co-signer if you have a limited credit history or a lower credit score. A co-signer’s good credit can strengthen your application.

Finally, understand the loan’s terms and conditions thoroughly before signing any agreement. Ensure you understand the repayment schedule, interest rates, and any associated fees.

{kind=link}