Understanding your credit score is paramount to achieving financial health. A strong credit score unlocks numerous financial opportunities, from securing favorable interest rates on loans and mortgages to obtaining credit cards with attractive rewards. Conversely, a poor credit score can significantly hinder your financial progress, leading to higher interest rates, limited credit access, and even difficulty securing employment in some cases. This article will explore the intricacies of credit scores, explaining how they’re calculated, what factors influence them, and most importantly, how you can improve yours to build a stronger financial future.

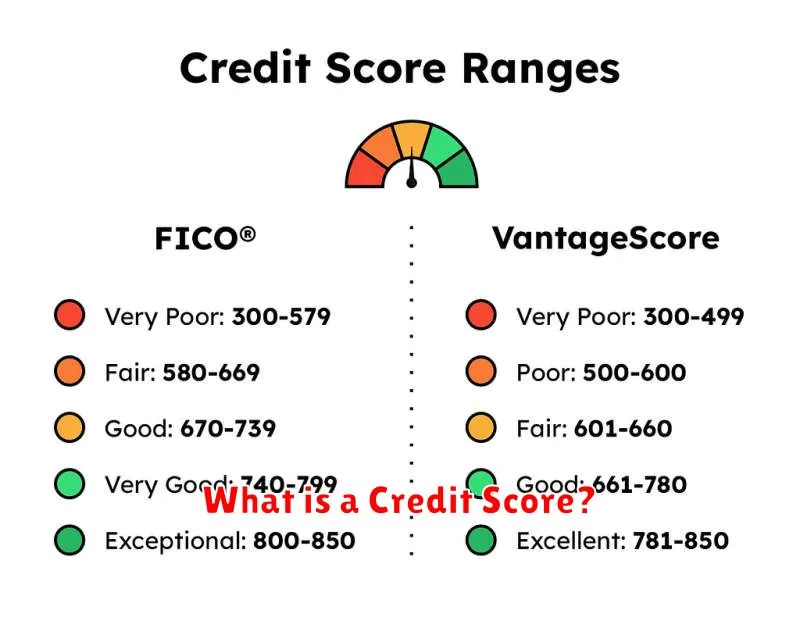

What is a Credit Score?

A credit score is a three-digit numerical representation of your creditworthiness. It’s a summary of your credit history, reflecting how reliably you’ve managed debt in the past.

Lenders use credit scores to assess the risk of lending you money. A higher credit score generally indicates a lower risk, making it easier to qualify for loans, credit cards, and other financial products with favorable terms (like lower interest rates).

Multiple credit bureaus (like Experian, Equifax, and TransUnion) independently calculate credit scores using a variety of factors. These factors include payment history, amounts owed, length of credit history, new credit, and credit mix.

Understanding your credit score is crucial for achieving financial health. It can influence not only your access to credit but also your insurance rates, employment opportunities, and even rental applications.

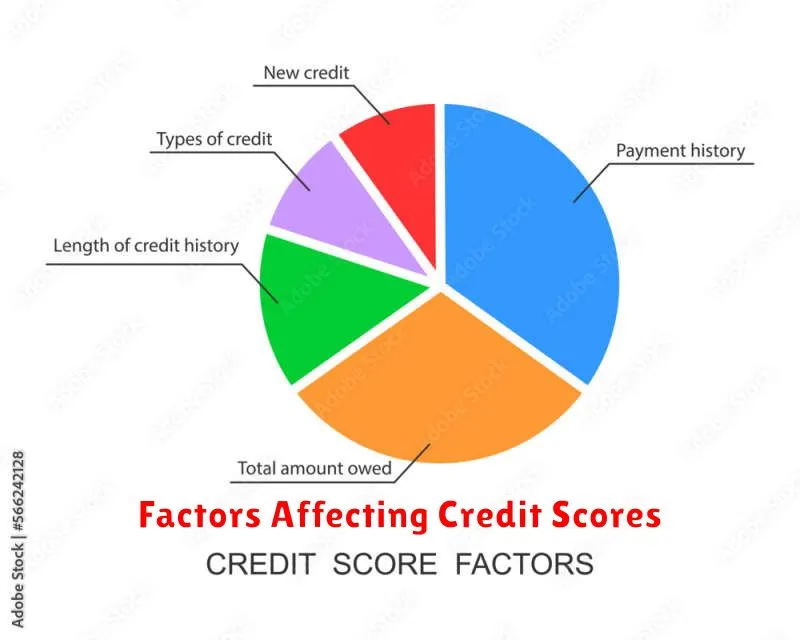

Factors Affecting Credit Scores

Your credit score, a crucial number impacting your financial life, is influenced by several key factors. Understanding these factors is essential for improving your score and securing favorable financial terms.

Payment History is the most significant factor, accounting for 35% of your score. Consistent on-time payments demonstrate financial responsibility. Even one missed payment can negatively impact your score.

Amounts Owed (30%) reflects your credit utilization ratio – the amount you owe compared to your available credit. Keeping this ratio low (ideally below 30%) signals responsible credit management.

Length of Credit History (15%) considers the age of your oldest and newest accounts. A longer history of responsible credit use generally results in a higher score.

Credit Mix (10%) refers to the variety of credit accounts you hold (e.g., credit cards, loans). A diverse mix suggests a broader understanding of credit management.

New Credit (10%) accounts for recent applications for credit. Multiple applications in a short period can temporarily lower your score as it suggests increased risk.

How to Improve Your Score

Improving your credit score requires consistent effort and responsible financial habits. Paying your bills on time is paramount; even one missed payment can negatively impact your score. Make every payment on time, every time.

Keep your credit utilization low. This means keeping your credit card balances well below your credit limits. Aim for less than 30% utilization, ideally much lower.

Don’t apply for too much credit at once. Each credit application results in a hard inquiry on your credit report, which can temporarily lower your score. Only apply for credit when truly necessary.

Maintain a mix of credit accounts. Having a variety of credit accounts (credit cards, installment loans) can demonstrate responsible credit management, but this should not be the primary focus. Prioritize responsible use of existing accounts.

Monitor your credit reports regularly. Check your reports from all three major credit bureaus (Equifax, Experian, and TransUnion) for errors and inaccuracies. Dispute any errors immediately.

Be patient. Improving your credit score takes time. Consistent positive actions will eventually lead to a higher score, but avoid focusing solely on the number. Focus on building good financial habits.

Importance of Credit History

Your credit history is a detailed record of your borrowing and repayment behavior over time. It’s a crucial factor in determining your credit score, a three-digit number that lenders use to assess your creditworthiness.

A strong credit history, demonstrating responsible borrowing and timely payments, is essential for securing favorable terms on loans, credit cards, and other financial products. Lenders view a positive history as a sign of low risk, leading to lower interest rates and better loan offers. Conversely, a poor credit history, marked by missed payments or defaults, can significantly restrict your access to credit and result in higher interest rates or loan denials.

Building a positive credit history takes time and responsible financial management. Regularly reviewing your credit reports for accuracy and paying your bills on time are key steps in maintaining a healthy credit profile. Your credit history is a valuable asset that impacts your financial well-being for years to come.

Impact on Loan Approvals

Your credit score is a crucial factor in determining loan approval. Lenders use it to assess your creditworthiness – your ability to repay borrowed money. A higher credit score indicates a lower risk to the lender, making it more likely that your loan application will be approved.

Conversely, a low credit score significantly reduces your chances of loan approval. Lenders may view applicants with poor credit history as high-risk borrowers, leading to loan rejection or the offering of loans with less favorable terms, such as higher interest rates.

The impact of your credit score extends beyond simple approval; it also affects the interest rate you’ll receive. A strong credit score typically qualifies you for lower interest rates, saving you considerable money over the life of the loan. A weak score often results in higher interest rates, increasing the overall cost of borrowing.

In summary, a good credit score is essential for securing favorable loan terms and improving your chances of loan approval. Maintaining a healthy credit score is a key step towards achieving your financial goals.

Managing Credit Effectively

Effectively managing your credit requires a proactive approach. Paying your bills on time is paramount; even a single late payment can negatively impact your score. Aim for on-time payments consistently.

Maintaining low credit utilization is crucial. This refers to the amount of credit you use relative to your total available credit. Keeping your credit utilization below 30% is generally recommended. Paying down balances regularly helps achieve this.

Diversifying your credit mix can also be beneficial. Having a variety of credit accounts, such as credit cards and installment loans (like auto loans), demonstrates responsible credit management to lenders. However, avoid opening numerous accounts in a short period.

Monitoring your credit report regularly is essential. Review your reports from all three major credit bureaus (Equifax, Experian, and TransUnion) for errors or discrepancies. Dispute any inaccuracies promptly.

Finally, understand that building a strong credit history takes time and responsible behavior. Be patient and persistent in your efforts. Consistent responsible credit management will ultimately lead to a better credit score and more favorable financial opportunities.

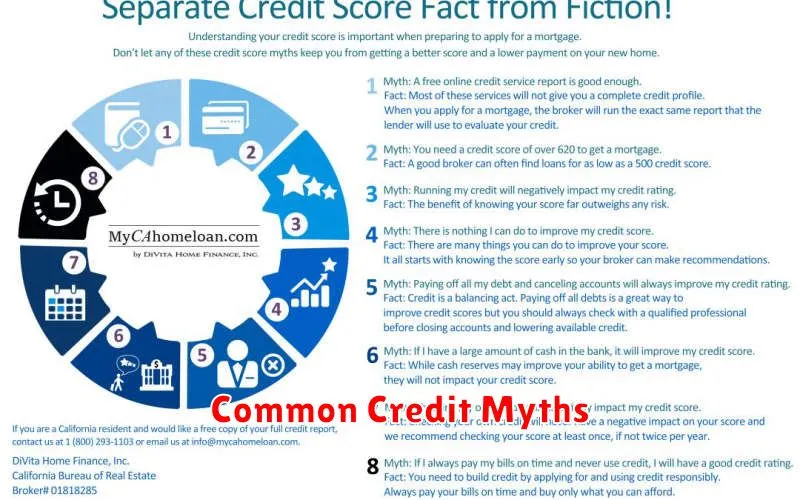

Common Credit Myths

Many misunderstandings surround credit scores. One prevalent myth is that checking your credit score lowers it. This is false; checking your score through authorized channels, like your credit card company or a credit bureau, has no impact.

Another common misconception is that only loans affect your credit. While loans significantly impact your score, other factors, such as credit card usage and timely payments on all debts, also play a crucial role. Your payment history accounts for a substantial portion of your credit score.

It’s also a myth that closing old credit accounts improves your credit. In fact, the length of your credit history is a key factor; closing old accounts can shorten this history, negatively affecting your score. An older account, even if unused, contributes to a stronger credit profile.

Finally, many believe that applying for multiple credit cards simultaneously won’t hurt your score. This is untrue; each application generates a “hard inquiry” which can temporarily lower your score. It’s best to apply for credit sparingly.

{kind=link}